You try getting an Assurance Vie company to accept that! We have been battling for several years on that issue.

Interesting! That makes them even less attractive.

Can’t you claim it back when you do your tax return?

1 Like

I agree with you that PEA are valuable options to consider for those seeking long term investments, albeit tax free gains are, inevitably, subject to 17.2% prélèvements sociaux.

Hypothetically, imagine you’re a French resident investor who has already put the maximum into tax favoured products such as Livret A, has put funds into PEA, which are capped, but still has additional funds to invest. The options for investment into other savings vehicles are pretty limited if you exclude AVs. I accept (and know all too well!) that charges can be high, but, for example, online providers who offer a fully managed investment service charge a maximum of 1.65% annually, which seems quite fair and reasonable to me. Plus some AV providers have literally hundreds of funds that people can invest in, there is no shortage!

My view is that AVs genuinely have their place, particularly if you are hypothetically in the (fortunate) position of having substantial funds available for investment, notwithstanding concerns about charges etc.

I haven’t looked into it, but I fear that there are other charges as well.

Plus managed services are usually not much good, and if they do beat the market, which they would have to by more than 1.65% to justify their charge, it’s more by luck.

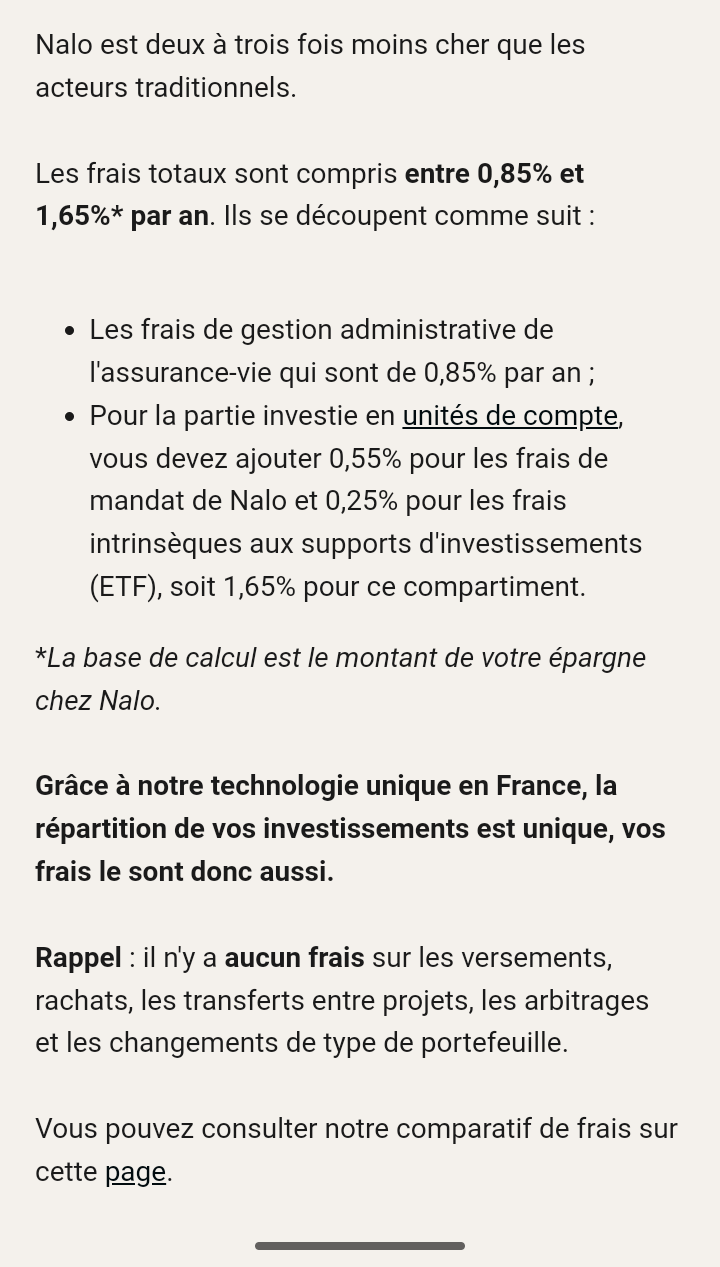

That is the maximum total charge for the online provider I use.

Out of interest, what is your basis for saying this - isn’t that quite a sweeping generalisation?! I’ve used managed investment services, both in France for AVs, and for the past 40 years in the UK, and think they perform a useful, and value added service for those of us who do not have the expertise, resources, confidence and time to appropriately manage their own investments.

Very clear and helpful.

Then I should be interested to know which one?

From reading financial magazines and reputable financial internet sites over the last 40 years.

We would prefer not to pay it to start with.

For others in a similar position, this is the attesation we used.

Attestation non régime SS français.pdf (240.7 KB)

2 Likes